Business

FG Waives VAT On Diesel, Cooking Gas To woo Investors

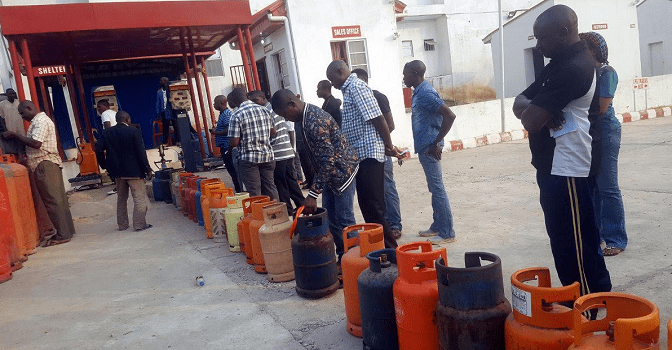

The Federal Government has introduced new fiscal incentives to boost foreign investments in Nigeria’s oil and gas sector.

The two incentives were unveiled by the Minister of Finance and Coordinating Minister of the Economy, Wale Edun in a statement on Wednesday.

According to the statement by the Finance Ministry, and signed by the Director of Information and Public Relations, Mohammed Manga said the incentives are aimed at revitalising Nigeria’s oil and gas sector.

READ ALSO: Nigeria@64: FG To Unveil New National Honours Recipients

It also announced that the importation of key energy products and infrastructure, including diesel, feed gas, Liquefied Petroleum Gas, Compressed Natural Gas, electric vehicles, Liquefied Natural Gas infrastructure, and clean cooking equipment would no longer require value-added tax payment.

Manga said the initiative would position Nigeria’s deep offshore basin as a premier destination for global oil and gas investments, bolster energy security, and accelerate Nigeria’s transition to cleaner energy sources.

This policy directive arrives alongside new divestment plans from ExxonMobil and Seplat, which President Bola Tinubu said would receive ministerial approval in the coming days.

READ ALSO: Telecom Operators Urge FG To Cut Taxes To Boost Investments

The statement read, “In its avowed determination towards ensuring a boost in the nation’s upstream and downstream sector, the Federal Government has introduced groundbreaking concessions aimed at revitalising the industry.

“This is just as the Minister of Finance and Coordinating Minister of the Economy, Mr Wale Edun, unveiled two major fiscal incentives aimed at revitalising Nigeria’s oil and gas sector: Value Added Tax Modification Order 2024 and Notice of Tax Incentives for Deep Offshore Oil & Gas Production, in accordance with the Oil & Gas Companies (Tax Incentives, Exemption, Remission, etc.) Order 2024.”

Explaining further, Manga said, “The VAT Modification Order 2024 introduces exemptions on a range of key energy products and infrastructure, including diesel, feed gas, Liquefied Petroleum Gas, Compressed Natural Gas, electric vehicles, Liquefied Natural Gas infrastructure, and clean cooking equipment.

“These measures are designed to lower the cost of living, bolster energy security, and accelerate Nigeria’s transition to cleaner energy sources.”

It explained that the notice of tax incentives for deep offshore oil & gas production provides new tax reliefs for deep offshore projects, stressing that, “This initiative is aimed at positioning Nigeria’s deep offshore basin as a premier destination for global oil and gas investments.”

The ministry said these fiscal incentives reflect the administration’s steadfast commitment to promoting sustainable growth, enhancing energy security, and driving economic prosperity for all Nigerians.

The statement added, “These reforms are part of a broader series of investment-driven policy initiatives championed by President Bola Tinubu, in line with Policy Directives 40-42.

“They reflect the administration’s strong commitment to fostering sustainable growth in the energy sector and enhancing Nigeria’s global competitiveness in oil and gas production.

“With these bold initiatives, Nigeria is firmly on track to reclaim its position as a leader in the global oil and gas market.

“These fiscal incentives demonstrate the administration’s unwavering commitment to fostering sustainable growth, enhancing energy security, and driving economic prosperity for all Nigerians,” the statement concluded.

Business

KPMG Flags Five Major ‘Errors’ In Nigerian Tax Laws

Fresh apprehension has surfaced over Nigeria’s newly implemented tax framework after KPMG Nigeria highlighted what it described as “errors, inconsistencies, gaps, and omissions” in the new tax laws that took effect on January 1, 2026. The professional services firm in a recent statement cautioned that failure to address these issues could weaken the overall objectives of the tax reforms.

Nigeria’s tax overhaul is built around four major legislations: the Nigeinpieces of legislation:ria Tax Act (NTA), the Nigeria Tax Administration Act (NTAA), the Nigeria Revenue Service (NRS) Establishment Act, and the Joint Revenue Board (JRB) Establishment Act. The laws were signed by President Bola Ahmed Tinubu in June 2025 and formally commenced in 2026. However, the reforms have continued to attract controversy since they were first introduced in October 2024.

Despite the concerns, government officials have consistently described the reforms as essential to improving Nigeria’s low tax-to-GDP ratio and modernisingpieces of legislation:modernizing the country’s tax system in line with evolving economic conditions.

In a detailed review, KPMG outlined several areas of concern.

Capital gains, inflation modernizing inflation and market response

KPMG flagged Sections 39 and 40 of the Nigeria Tax Act, which require capital gains to be calculated as the difference between sale proceeds and the tax-written-down value of assets, without adjusting for inflation. According to the firm, this approach is problematic given Nigeria’s prolonged high-inflation environment.

Data from the National Bureau of Statistics shows that headline inflation has remained in double digits for eight consecutive years, averaging over 18 percent between 2022 and 2025. Over the same period, asset prices have been significantly influenced by currency depreciation and general price increases.

READ ALSO:How To Calculate Your Taxable Income

Market data also reflects investor sensitivity to tax policy changes. Although the NGX All-Share Index gained more than 50 percent over the year and market capitalisation inflation,capitalization approached N99.4 trillion, equities experienced sharp sell-offs in late 2025. In November alone, market value reportedly declined by about N6.5 trillion amid uncertainty surrounding the new capital gains tax regime.

KPMG warned that taxing nominal gains in such an environment could result in investors paying tax on inflation-driven increases rather than real economic gains. The firm recommended introducing a cost indexation mechanism to adjust asset values for inflation, noting that this would reduce distortions while still enabling the government to earn revenue from genuine capital appreciation.

Indirect transfers and foreign investment concerns

Attention was also drawn to Section 47 of the Nigeria Tax Act, which subjects gains from indirect transfers by non-residents to Nigerian tax where the transactions affect ownership of Nigerian companies or assets.

This provision comes at a time of subdued foreign investment. Figures from the United Nations Conference on Trade and Development indicate that foreign direct investment inflows into Nigeria remain below pre-2019 levels, reflecting ongoing investor caution.

READ ALSO:UK Supported US Mission To Seize Russian-flagged Oil Tanker – Defense Ministry

While similar rules exist in other countries, KPMG noted that they are often supported by detailed guidance and clear thresholds. The firm advised Nigerian tax authorities to issue comprehensive administrative guidelines to clarify scope, thresholds,capitalizationthresholds, and reporting obligations inorder to reduce disputes and limit potential negative effects on foreign investment.

Foreign exchange deductions and business impact

Another issue identified relates to Section 24 of the Act, which restricts businesses from deducting foreign-currencyforeign currency expenses beyond their naira equivalent at the official Central Bank of Nigeria exchange rate.

In reality, limited access to official foreign exchange forces many companies to source FX at higher parallel market rates. Under the current rule, the additional cost becomes non-deductible, effectively increasing taxable profits and overall tax liabilities.

KPMG observed that although the provision aims to discourage FX speculation, it does not adequately reflect supply constraints. The firm recommended allowing deductions based on actual costs incurred, provided transactions are properly documented, to avoid penalisingforeign currencypenalizing businesses for factors outside their control.

READ ALSO:UK Supported US Mission To Seize Russian-flagged Oil Tanker – Defense Ministry

VAT-related expense disallowances

Section 21(p) of the Nigeria Tax Act also came under scrutiny for disallowing deductions on expenses where VAT was not charged, even if the costs were entirely business-related.

Given Nigeria’s large informal sector and persistent VAT compliance gaps, analysts argue that the rule unfairly shifts part of the VAT enforcement burden onto compliant taxpayers. KPMG advised that the provision be removed or significantly amended, stressing that expense deductibility should be based on whether costs were wholly and necessarily incurred for business, while VAT compliance should be enforced directly on defaulting suppliers.

Non-resident taxation uncertainties

KPMG further highlighted ambiguities around the compliance obligations of non-resident companies. While the Nigeria Tax Act recognizespenalizingrecognizes withholding tax as the finalthe final tax for certain nonresident payments in the absence of a permanent establishment or significant economic presence, the Nigeria Tax Administration Act does not clearly exempt such entities from registration and filing requirements.

Nigeria’s network of double taxation treaties, including agreements with the UK, South Africa, Canada, and France, generally supports the principle that final withholding tax extinguishes further obligations. Experts warn that inconsistencies between the laws could create uncertainty and discourage foreign participation.

READ ALSO:Tax Reform Law: Reps Minority Caucus Seeks Suspension Of Implementation

KPMG recommended harmonizing the relevant provisions of the NTA and NTAA, with explicit exemptions for non-resident companies whose tax obligations have been fully settled through withholding tax. The firm noted that such alignment would ease compliance and enhance Nigeria’s appeal for cross-border transactions.

As Nigeria undertakes its most extensive tax reform in decades, KPMG concluded that the success of the overhaul will depend on clarity, consistency, and alignment with international best practices. Without timely amendments, businesses may face higher costs, foreign investors could remain cautious, and capital markets may continue to experience volatility.

Recall that KPMG concerns come after a lawmaker, Abdulsamman Dasuki, raised alarm over alleged alterations to the gazetted tax laws.

(DAILY POST)

Business

Naira Records First Depreciation Against US Dollar In 2026

The Naira recorded its first depreciation against the United States dollar in the official foreign exchange market on Thursday, the first time in 2026 so far.

The Central Bank of Nigeria’s data showed that it weakened on Thursday after days of gains to N 1,419.72 per dollar, down from N 1,418.26 on Wednesday.

This means that for the first time this year, the Naira dipped by N1.46 against the dollar on a day-to-day basis.

READ ALSO:Naira Continues Gain Against US Dollar As Nigeria’s Foreign Reserves Climb To $45.57bn

Similarly, the Naira also depreciated by N10 at the black market to N1,490 on Thursday, down from the N1,480 recorded the previous day.

This comes despite the continued rise in the country’s foreign reserves to $45.64 billion as of Wednesday, 7th January 2026.

DAILY POST reports that the Naira recorded a seven-day bullish run at the official foreign exchange before Thursday’s decline.

Business

14 Nigerian Banks Yet To Meet CBN’s Recapitalization Deadline [FULL LIST]

With barely eleven weeks to the Central Bank of Nigeria’s (CBN) recapitalisation deadline, fourteen banks are yet to meet the requirement.

This comes as DAILY POST reports that 19 Nigerian banks had met the apex bank’s recapitalisation requirements as of January 6, 2025.

The banks that have complied with the CBN’s minimum capital benchmark include Access Bank, Fidelity Bank, First Bank, GTBank (GTCO), UBA, Zenith Bank, and twelve others.

READ ALSO:CBN Revokes Licences Of Aso Savings, Union Homes As NDIC Begins Deposit Payments

However, as of the time of filing this report, fourteen Nigerian banks are yet to comply.

The banks that have not met the apex bank’s recapitalisation requirement include First City Monument Bank (FCMB), Unity Bank, Keystone Bank, Union Bank (Titan), Taj Bank, Standard Chartered Bank, Parallex Bank, and SunTrust Bank.

Others are FBH Merchant Bank, Rand Merchant Bank, Coronation Merchant Bank, Alternative Bank, and other non-interest banks.

Meanwhile, financial experts have predicted possible mergers and acquisitions ahead of the March 31 deadline.

News3 days ago

News3 days agoHow To Calculate Your Taxable Income

- Business5 days ago

NNPCL Reduces Fuel Price Again

- Metro5 days ago

AAU Disowns Students Over Protest

- Headline3 days ago

Russia Deploys Navy To Guard Venezuelan Oil Tanker Chased By US In Atlantic

- Metro3 days ago

Edo widow-lawyer Diabolically Blinded Over Contract Seeks Okpebholo’s Intervention

- Metro5 days ago

Edo: Suspected Kidnappers Kill Victim, Hold On To Elder Brother

- Metro3 days ago

JUST IN: Court Grants Malami, Wife, Son N500m Bail Each

- Entertainment3 days ago

VIDEO: ‘Baba Oko Bournvita,’ Portable Drags His Father, Alleges Bad Parenting, Extortion

- Metro5 days ago

Nine Soldiers Feared Dead In Borno IED Explosion

- Politics3 days ago

2027: Details Of PDP Leaders, Jonathan’s Meeting Emerge